Today's Market News:

Sales Accelerate, Then Rates Hit the Brakes

Having trouble keeping up with housing market stats? You're not alone. While the number of closed home sales rose in May, pending home sales during the same month were flat.

U.S. existing home sales jumped 2.8% month-over-month in May, rising to their highest level since October 2022. Overall sales of both existing and new homes also rose to their highest level since October 2022, rising 3.8% month-over-month.

However, while closed sales surged, pending sales flattened as mortgage rates rose. These are considered a more current market indicator. In addition, economic and global uncertainty contributed to deterring would-be home buyers.1

More Sellers Hit Pause

Consumer confidence is having a rough spring, and it continues to affect the housing market. More home sellers are delisting their properties, with 5.8% of national listings pulled off the market in April.

Atlanta, Georgia saw the highest share of delisted homes in April, with 1 in 10 removed. San Jose, California, followed with roughly 9% pulled, then Los Angeles, California (7.8%), Dallas, Texas (7.8%) and Seattle, Washington (7.7%).

Nervous sellers are choosing to take a break as higher mortgage rates, elevated gas prices and weaker consumer confidence continue to take their toll on housing demand. In addition, sellers are no longer in the driver's seat in many areas and some have realized they probably won't get the price they expected.

A Redfin agent commented: "Buyers know they have negotiating power, often offering under the asking price and completing inspections, but some sellers just won't budge."2

Gen Z: Buying On Their Own Terms

While Generation Z (ages 18 to 26) accounted for just 4% of home buyers during 2025, their impact on the housing market is expected to grow in the years ahead. Working with Gen Z prospects will probably feel different than working with older prospects. Here are some reasons why.

Gen Z isn't postponing home ownership until they reach one of life's traditional milestones. Marriage and children are not mandatory. According to NAR's most recent Home Buyer Households research, 53% of Gen Z buyers purchased homes solo, and 35% were single women — the highest share of single female buyers across all generations. Another 17% were unmarried couples, also the highest of any generation.

Their reasons for buying were different than those seeking stability for a family. NAR's 2026 survey found that 39% of Gen Z buyers bought a home simply because they wanted one of their own. Over 70% considered their decision to be a good financial investment, with 30% saying it's better than stocks.

Since Gen Z buyers are still building careers, affordable properties are often limited to condo units, townhomes, and rowhouses. As always, feel free to pass on my contact information to these prospects.3

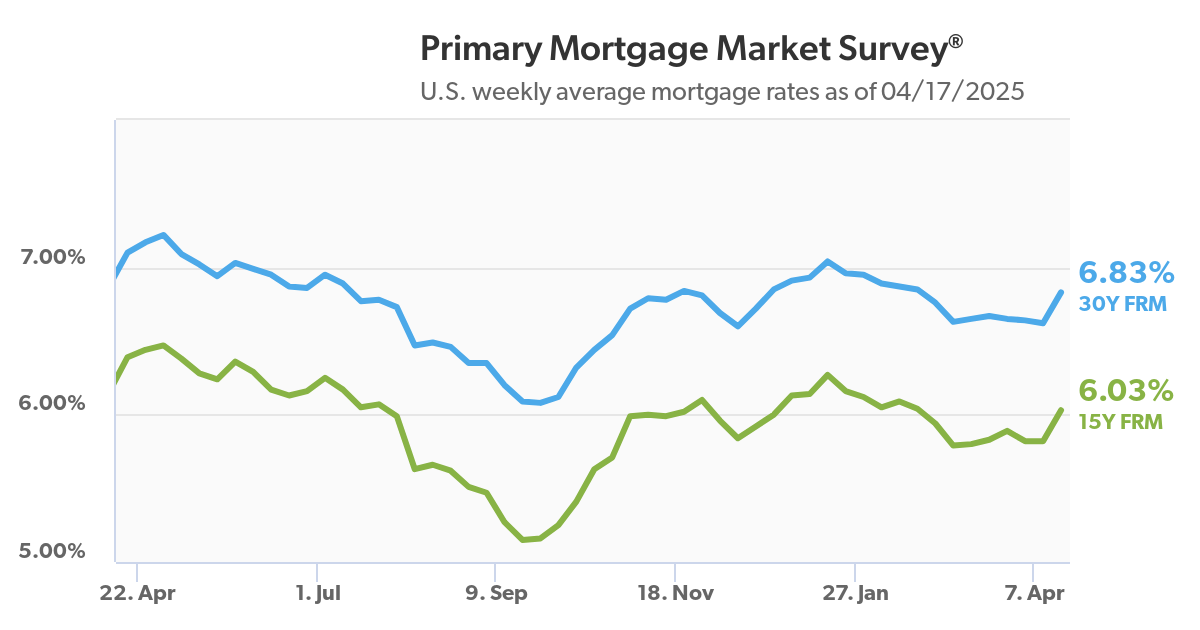

Why Adjustable-Rate Mortgages Are Becoming More Popular

Adjustable-rate mortgages (ARMs) accounted for nearly 21% of mortgage originations in 2025. Even though the 30-year fixed-rate mortgage has been popular for decades, ARMs can be problem-solvers for some home buyers.

Instead of committing to a fixed rate for decades, some borrowers are opting for ARMs as a short-term strategy. Some expect interest rates to fall further and plan to refinance later, while others prioritize immediate payment relief over long-term certainty.

While 30-year fixed rates have fallen to around 6.1% in early 2026, a typical 5/1 ARM sits near 5.3%, providing buyers with a lower monthly payment for several years.

For example, a California buyer who needs $1 million in financing may qualify for an ARM offered at 5.3% while a 30-year, fixed-rate mortgage is offered at around 6.1%. This 0.8-percentage point difference can reduce the buyer's monthly payments by nearly $500.

High-cost housing markets are seeing more ARMs, especially in California, Washington, D.C., and Massachusetts. In these and other high-cost regions, they're providing an alternate path to affordability.4

Manage Negative Reviews for Positive Results

Here are some basics to keep in mind.

Be empathetic. Apologizing for their negative experience and expressing empathy can help you de-escalate a situation and even create a rapport with a customer.

Clarify the problem. Before you can provide a solution, you'll need to understand what happened, and what would make the customer feel better. Ask questions like "Can you talk me through what happened?"

Listen carefully. The customer may take longer to explain the problem than you expected, so be patient. Using phrases like "I understand," and "That makes sense" assures them you're taking them seriously.

Offer solutions. For example, if a seller client is unhappy with how their listing is being marketed, ask them how it can be improved. Other problems, such as pricing disagreements, may require a review of the CMA.

Following up a few days later can reframe a service interaction as a positive customer experience and even turn an unhappy buyer or seller into a referral source.5

Sources: 1redfin.com, 2cnbc.com, 3nar.realtor, 4nationalmortgageprofessional.com, 5shopify.com

Recent Comments