Rejected FHA Borrowers Get Another Chance

If you've ever lost a sale because your buyer clients were rejected for FHA financing, here's a great reason to reach out to them. Now these borrowers can re-apply for FHA financing without running into the Mortgage Credit Reject (MCR) screen formerly faced by lenders and underwriters.

This also means that, if another lender recently rejected their FHA application, I can review their financial details with my support staff and see if there's a way to approve them sooner than later.

Formerly, when a would-be home buyer was rejected for FHA financing, they were unable to re-apply with that lender for six months. If another lender reviewed the rejected application, a review by a Homeownership Center (HOC) would be mandatory. The HOC review would not guarantee approval.

FHA officials described the elimination of the MCR status as follows:

"FHA has determined that this flag does not improve risk management and is often why other lenders will reject an applicant even when that applicant might otherwise qualify for a loan."1

Generation Z: Plugged-In and Pessimistic

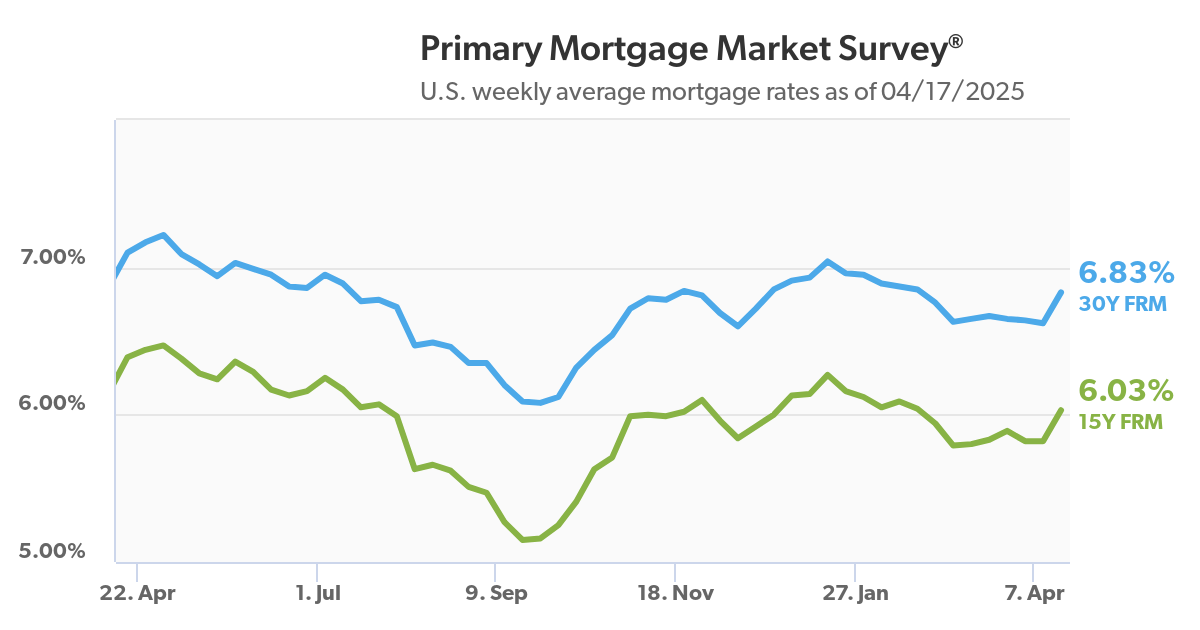

Affordability has become a major speed bump for many would-be homeowners, and members of Generation Z (aged 18 to 26) are feeling it as much as anyone else.

A recent Qualtronics survey of 1,340 Gen Z participants (aged 18 to 26) asked them if they planned to buy a home soon or continue renting. While some are pursuing additional work to help save for a down payment, around 10% don't think they'll ever buy a home. While the second most common response was the inability to produce a down payment, even more claimed that homes simply weren't affordable. Only 13% claimed they weren't interested.

The other age group that took part in the survey, Millennials, gave similar answers to Gen Z participants.

- About 30% of both groups said that mortgage rates in June 2023 were too high for them to consider home ownership.

- About 20% of the Gen Zers and 16% of Millennials planned to pay off their student loans before they would consider home ownership as something they could afford.

- Roughly 40% of both groups admitted they were working side hustles so they could buy sooner than later.

- 25% had been promised cash from family members to help with the down payment, while roughly 15% plan to sell cryptocurrency.2

Add Home Inspector to Your Skill Set

It never hurts to add a new certificate to your wall, especially during times when inventory is low. As home inspectors play a critical role in many transactions, it's something you may want to look into.

Home inspectors check for flaws in electrical systems, plumbing, HVAC, windows, doors, foundations, basements, attics and roofs before preparing a report. Buyers who hire inspectors will have additional information about their purchase before making a final decision.

Becoming an inspector always begins with researching your state's requirements. Click here for a national map with links to every state. These vary widely from one state to another, with 14 states not requiring certification.

Next, you'll go through these steps (if and when applicable to your state):

- Complete your pre-licensing education. These may be online or classroom courses.

- Pass your licensing exam. Most states that require an exam will direct you to the National Home Inspector Examination (NHIE).

- Check for additional requirements. These may include proof of insurance, and/or a number of ride-along inspections with a licensed inspector.

- Complete your state's application. Keep up with post-licensing requirements. These may include Continuing Education (CE) and other forms of professional development. By now, you should be familiar with your state's resources for inspectors.

Real estate agents often make excellent home inspectors for several reasons: their attention to detail, ability to write concise reports, and understanding that integrity is vital.3

Remote Properties for Remote Workers

While a few companies are planning to bring their remote workforce back to the office, there are many more who have given their blessing to staff who prefer to work from home. These workers save on commuting costs, with many also saving on childcare (which is prohibitively expensive in some cities), while the employers save big by downsizing their commercial offices.

When shopping for their next home, remote workers have another attractive option open to them: buying in less popular locations.

While location still plays a big part in a home's value, one overlooked reason is supply and demand. Not everyone is able to work remotely, and not every worker prefers it. Therefore, demand for properties that shorten commuting times is still bigger than for homes without this feature. And many remote workers initially prefer these homes as they don't fully realize their options.

Some conversation starters with a potential buyer could include their future career expectations and favorite outdoor pursuits. Some topics to bring into the conversation:

- Homes that aren't in the commuter belt will be priced accordingly, which could offer the buyer more affordable choices.

- Moving to a rural area would provide a quieter area for working at home, which could increase productivity. It could also bring outdoor activities conveniently closer, enhancing work-life balance.

- If there's new construction further out of town, the buyer could choose custom features, and many builders are offering buy-downs to make their homes more affordable.4

Renovations That Reduce ROI

Whenever you're talking home values with a client — whether it's an established buyer, or a potential client who's thinking of selling — renovations are often a topic. And since you have experience showing homes, you'll know which renovations help sell a home, and which don't.

This is when you may earn lasting loyalty by advising them against some home improvements. Even though some future sellers may think they're boosting their ROI (Return on Investment), they may be doing exactly the opposite.

This is when you may earn lasting loyalty by advising them against some home improvements. Even though some future sellers may think they're boosting their ROI (Return on Investment), they may be doing exactly the opposite.

Here are three that often dampen potential buyers' interest, and why:

Excessive electronic personalization. Even though most homeowners own flat-screen televisions, gaming systems and virtual assistants (Alexa and similar), chances are they won't be bringing identical items. This means a buyer will probably spend hours, if not days, removing and replacing these.

Carpeted floors. Even a brand-new carpet can be off-putting for several reasons. For families with children and/or pets, keeping it clean will be a major chore. Viewers with asthma or allergies are recommended to avoid carpeting because of the difficulty of keeping it free of dust and allergens. Roomba-ready wood floors are currently the #1 pick for decorators and homeowners alike.

In-ground swimming pools. Unless every other home on the street has an in-ground pool, these can be deal-killers. Not only do they need regular, sometimes-expensive maintenance, but some families will worry about the potential risk to amateur swimmers.5

Sources: 1nationalmortgageprofessional.com, 2redfin.com, 3theclose.com, 4lightersideofrealestate.com, 5lifehacker.com

Recent Comments