How To Keep Selling in a Down Market

Even if you're relatively new to real estate, you're probably aware of its cyclical nature. However, the current market atmosphere isn't the entire story.

Some agents close plenty of sales every month, even in a down market. This is because they know that success depends on making visibility, customer relationships and education part of their daily tasks. Let's take a closer look at each.

In a down housing market, visibility is crucial. Prospects need to know that you're as committed to your real estate community as ever. Consistent social media activity is the best way to enhance your visibility. Share insights about what's going on in your territory, and post tips for buyers and sellers that encourage them to act.

A strong Customer Relationship Management (CRM) system is your secret weapon, as you'll be able to nurture existing relationships while generating new leads. Your CRM helps you organize contacts, track interactions and set follow-ups. This ensures consistent, reassuring connections with clients.

To thrive in a slower market, be an expert in your field. Research its history, study future trends, and attend industry conferences. The better prepared you are to negotiate a complicated down market, the more your prospects will trust you.

While our business is always evolving, there are key tools that will help you succeed in any market. Remember, I'm always here to assist you and your clients.1

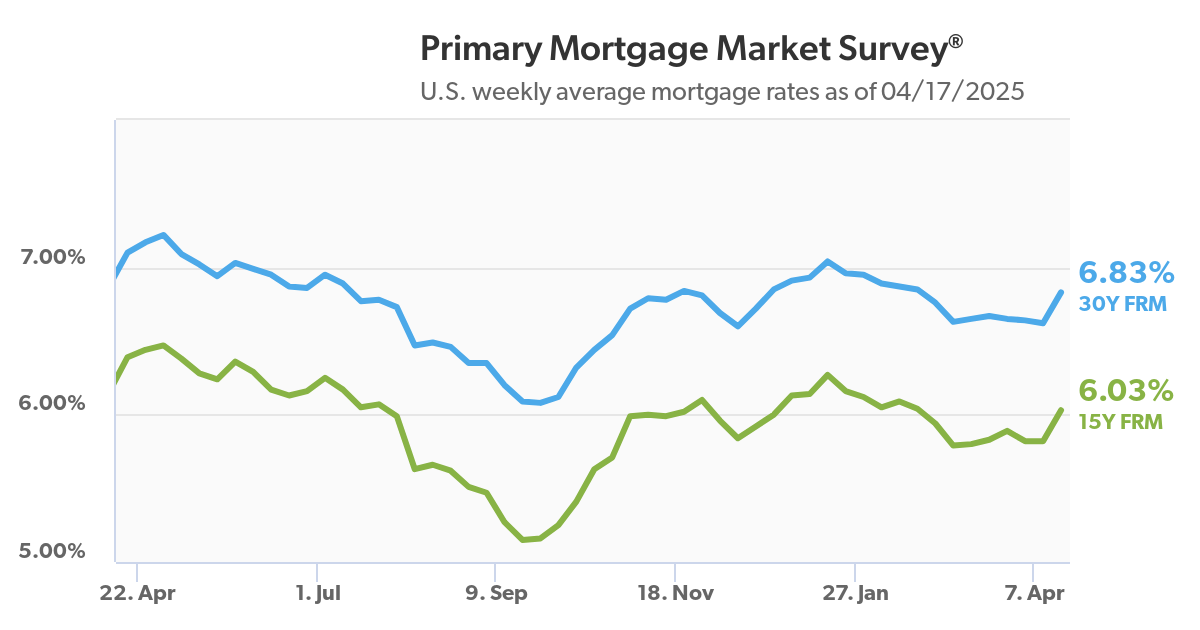

Fix High Rates With an ARM

While most buyers choose the standard 30-year, fixed rate mortgage, an adjustable-rate mortgage (ARM) can be a smart alternative, especially when rates are rising...like now.

While rates for fixed-rate mortgages continue to climb, rates for ARMs have fallen. According to the Mortgage Bankers Association's index, our market recently saw a run on ARMs that pushed mortgage application volume higher.

Earlier this month, the average rate for the 30-year, fixed-rate loan increased from 7.53% to 7.67% for buyers putting 20% down. But average rates for 5/1 ARMs fell from 6.49% to 6.33%. This caused loan applications for new purchases to rise by 1%.

If you're unfamiliar with ARMs, give me a call and I'll go over the basics with you, including the types of buyers who could be a good fit for this loan.2

Banking Group Proposes Solution to High Rates

Home buyers aren't the only ones unhappy with current mortgage interest rates. Last week, The Independent Community Bankers Association (ICBA) began promoting a plan that could reduce mortgage interest rates by 1% to 1.5%.

The ICBA was supported by the National Association of Realtors (NAR), and Community Home Lenders of America. Together, these three submitted a letter to The White House and Treasury Department outlining a plan to reduce the historically large spread between 30-year mortgage rates and 10-year Treasuries.

ICBA states that their proposal could reduce mortgage rates by up to 150 basis points. They also recommended that the following changes take place:

- The Federal Reserve shift its policy to maintain its stock of mortgage-backed securities (MBS), suspending runoff until the spread between the 30-year fixed rate mortgage and 10-year Treasury note stabilizes.

- Enable Fannie Mae and Freddie Mac to purchase their own MBS and/or Ginnie Mae MBS for a temporary period of time.

How to become a LinkedIn Top Voice

Many social media platforms are rethinking the way they reward their top creators. While some are providing training for certain brand certificates, such as Facebook/Meta, you'll have to pay to take the exam and earn your badge.

LinkedIn has taken a different approach. Top Voices badges are awarded to members "to make it easier to identify and follow valued and quality content on LinkedIn."

The blue Top Voice badge is reserved for "senior-level experts and leaders". They're chosen by the LinkedIn Editorial team, who reward those who build their brand and increase their following by creating and publishing high-quality content.

Here are the steps required to earn your badge.

- Make sure your LinkedIn profile is complete.

- Define your audience. Who are you talking to, and what problems can you help them solve?

- Produce helpful, engaging content and publish a fresh article every week. It's especially helpful to share tips and strategies that establish you as a problem-solver within the real estate industry.

- Build trust by sharing your own experiences, even the mistakes you've made earlier in your career.

- Engage with other LinkedIn creators, commenting on their posts in a thoughtful, helpful manner.4

First-Time Buyers and Parental Gift Funds

Depending on the comfort levels you share with your first-time buyers, you may want to ask them if The Bank of Mom and Dad would be willing to help them with their down payment, closing costs, or both.

Saving for a down payment can take years, but cash provided as gift funds can speed up that process. Younger buyers are currently making the most parental ATM withdrawals, with 78% of Generation Z homeowners reporting some financial support for a down payment, mostly from their parents. 54% of Millennials have received assistance, followed by 33% of Gen Xers.

Since this type of assistance needs to be carefully documented as gift funds, feel free to refer your first-time buyers to me so I can make sure they're aware of their options.5

Sources: 1housingwire.com, 2cnbc.com, 3nationalmortgageprofessional.com, 4buffer.com, 5themreport.com

Recent Comments