Today's Market News:

Interest Rates Rise to Highest Level in 11 Months

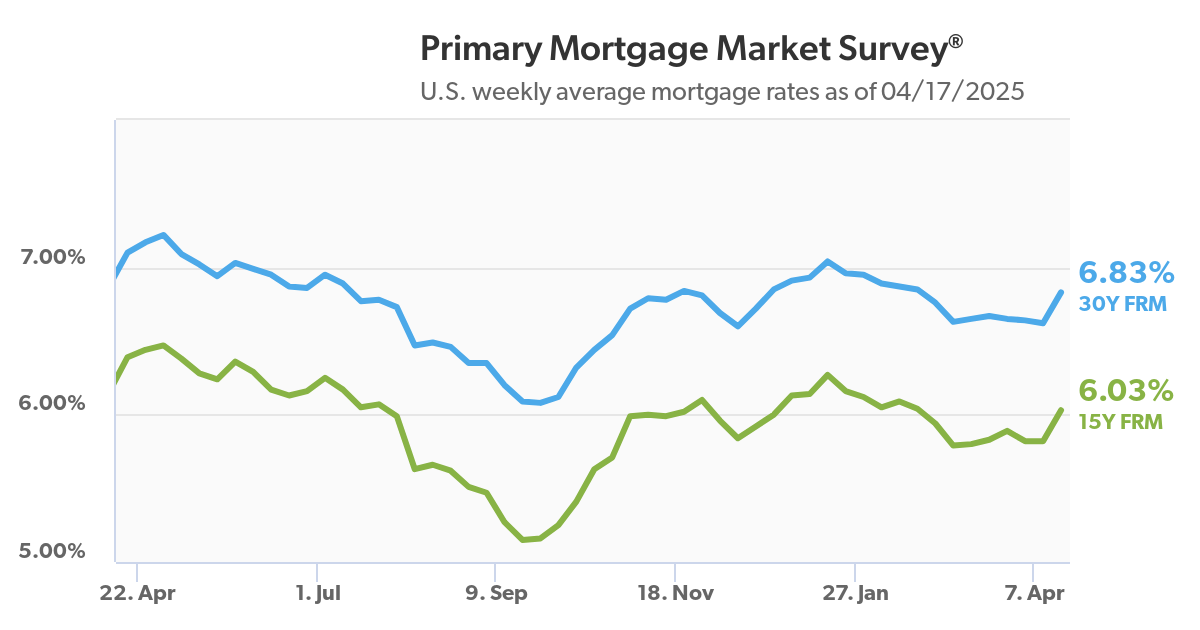

Last week's mortgage rates rose to 6.65%, which is the highest level since August 2025. This, combined with rising home prices, resulted in fewer prospective home buyers applying for financing.

Total mortgage application volume dropped 2.7% last week* when compared with the previous week.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances, $832,750 or less, increased to 6.65% from 6.58% last week, with points rising to 0.67 from 0.64, including the origination fee, for loans with a 20% down payment.

Applications for new purchase mortgages fell 7% from the previous week and were 2% lower than the same week one year ago. Buyers are still faced with high home prices as well as a limited number of affordable homes for sale in some areas.

* According to the Mortgage Bankers Association's seasonally adjusted index, this statistic is for the week ending July 10th, 2026.1

Home Prices Hit a New High

Prices rose 2.2% year-over-year in June to a record high, fueled mainly because of growing demand.

Existing U.S. home sales ticked up to a seasonally adjusted annual rate of 4.4 million, the highest level since 2022. Pending home sales reached their second-highest level since 2023.

Wealthy Bay Area and South Florida buyers helped fuel both home-price and sales increases. Sale prices rose 9% year-over-year in both San Francisco and West Palm Beach, and closed home sales posted increases of roughly 23% in both metros.

New listings trended down, declining 1% month-over-month to their lowest level since December. Some of the nation's strongest buyers' markets had the biggest decline in listings, led by Dallas, TX (-6.5%), Fort Worth, TX (-6.2%), and Jacksonville, FL (-5.5%).2

NAR Issues Guidance on Office-Exclusive and Pre-Market Listings

NAR recently published a new four-page resource, Office Exclusive Listings / Pre-Marketing Guidance.

Office-exclusive listings are defined as filed with the MLS and shareable with agents inside the listing firm depending on the listing contract. They are not publicly marketed or shared with MLS participants or subscribers outside the firm.

Pre-marketing: options like Coming Soon statuses and Delayed Marketing Exempt Listings (DMEL) are "set locally" — each MLS decides which it offers and under what rules.

NAR's Guidance explains how these listing types work, together with brokers' responsibilities.

Key rules discussed include the following:

- The seller decides how much exposure their listing gets, based on their own priorities.

- Brokers must walk sellers through their options, explaining how each one fits the seller's goals and serves the seller's best interest.

- Brokers are responsible for paperwork. Once a seller opts for an office-exclusive or pre-marketing route, the broker needs a signed disclosure covering the agent-seller relationship; the MLS benefits the seller is giving up, and confirmation the listing won't be publicly marketed.

- MLS rules still apply. NAR stated that enforcement "is the responsibility of the local MLS."

The full document is available as a PDF. Click here to view and download the entire guide.3

June Home Sales Lower Than Expected

Sales of previously owned homes in June dropped 2.4% from May to 4.09 million units on a seasonally adjusted, annualized basis, according to data provided by the National Association of REALTORS®. Home sales were down in every region except for the Northeast.

The median price of an existing home sold in June was $440,600, an increase of 1.8% from the year before and the highest on record. June is usually one of the strongest months for both sales and prices.

Sales continue to be strongest at the higher end of the market. Sales of homes priced between $100,000 and $250,000 were up less than 1%, while sales of homes priced between $750,000 and $1 million were up nearly 14% from the year before.4

ROAD to Housing Changes Ahead

The FHFA will be updating the Uniform Residential Loan Application within six months, informing qualified military veterans of their eligibility for a VA Home Loan if they (or a deceased spouse) served, or are serving in the U.S. Armed Forces. This will appear above the signature line.

Local governments are encouraged to expedite permitting, support commercial-to-residential conversions, and increase housing production. You'll want to monitor permit activity, planning-board agendas, ADU ordinances, and redevelopment proposals as they appear.

Appraisal review procedures may change. The FHA, FHFA, Dept. of Veterans Affairs and Dept. of Agriculture must maintain procedures for borrowers seeking a Reconsideration of Value. Agents can prepare by keeping accurate comparable sales, improvement records, permits, concessions, and evidence of factual errors.

Investor purchase restrictions begin January 7th, 2027. Since this law only restricts purchases of single-family homes by entities that control at least 350 properties, your investor clients will probably not be affected.

Since these have different implementation schedules, you'll need to confirm each one before sharing details with prospects. Feel free to contact me with questions.5

Sources: 1cnbc.com, 2redfin.com, 3realestatenews.com, 4cnbc.com, 5theclose.com.

Recent Comments