Today's Market News:

Buying Power Continues to Rise

A recent Zillow analysis found that a median-income household can now afford a home priced at $331,483. This adds up to a $30,302 increase in buying power since last year, and the highest affordable price since March 2022.

Buyers who put down a 20% down payment may be able to qualify for monthly mortgage payments (excluding taxes and insurance) that are over 8% lower than a year ago.

Buyers shopping in cities with more expensive properties will see bigger boosts in buying power. San Jose, California buyers in median-income households have gained almost $74,000 in buying power from a year ago, while Boston buyers in median-income households have gained around $46,390 in buying power during the past year.

Prospective buyers may fare even better in markets where home values have fallen, including Dallas and Houston, Texas; Phoenix, Arizona; Miami, Florida and Atlanta, Georgia.1

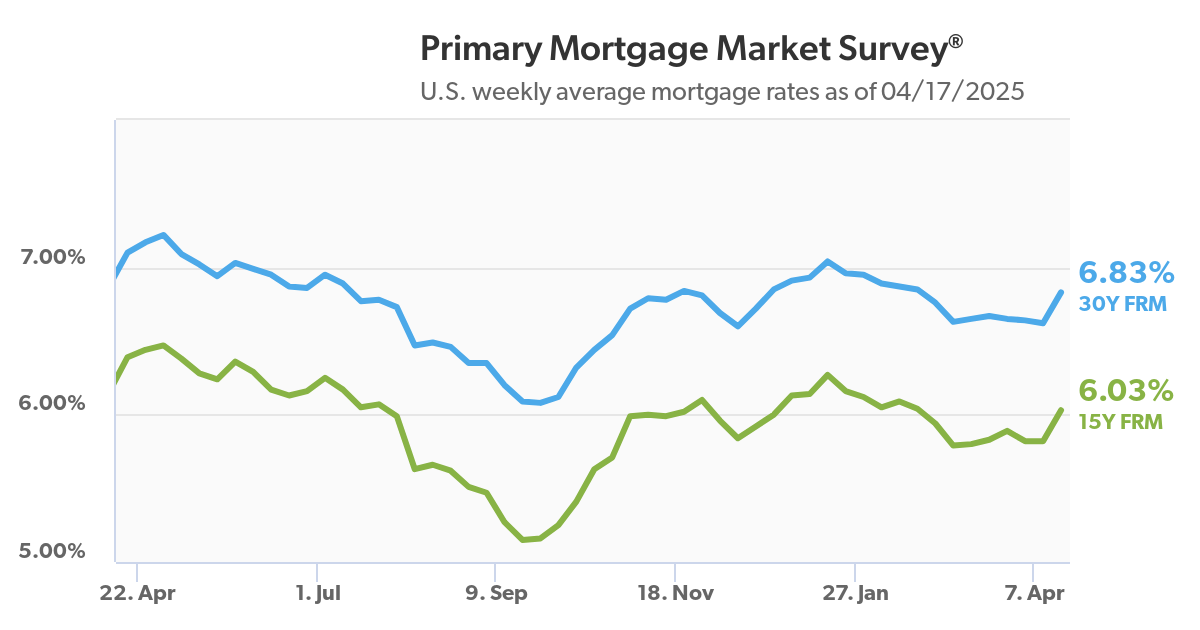

Mortgage Rates Fall Below 6%

Recent economic news triggered a drop in 30-year mortgage rates. According to Mortgage News Daily, 30-year, fixed-rate loan rates fell to 5.99%. While rates briefly dipped into the 5% range for a few hours in January, they bounced back that same day. Another, similar rise is unlikely now, according to the CEO of Mortgage News Daily.

Lower rates are a positive sign, especially as the spring housing market isn't that far away. For example, a buyer putting 20% down on the median priced home, about $400,000 according to the National Association of Realtors® (NAR), would have a monthly payment of $1,916 for the principal and interest. One year ago, that payment would have been $2,105, a difference of $189.

In addition, NAR's Lawrence Yun pointed out that: "With mortgage rates nearing 6%, an additional 5.5 million households that could not qualify for a mortgage one year ago would qualify at today's lower rates."2

Slow Market or Spring Training?

Whether you're a new agent or a top-selling sales veteran, you may feel stressed when the real estate market hits a speed bump. But it's better to view downtime as an opportunity to prepare for the busier days ahead. Think of yourself as an athlete — even though it's not game time all the time, spring training is essential. You'll be in top sales shape when the spring real estate market arrives.

- Double down on prospecting with traditional methods, such as personally calling every lead that's called you during the past six months.

- Visit previous clients in person with a small gift or premium item. This can help generate referrals while helping you feel less isolated.

- Find new ways to be useful within your community, such as volunteering. This is a softer approach to networking and prospecting.

- Revisit your business plan and identify what worked the best. This may require reviewing your CRM system or marketing campaigns.

- Get non-sales tasks out of the way, such as completing any required Continuing Education (CE) courses.

- Take a break if possible. Recharging your mindset is productive, too. This industry demands energy, so vacations aren't luxuries; they're essential.

Why Buyers' Credit Reporting Costs Are Rising

Even though mortgage rates have fallen slightly this year, some related costs have risen. One that's getting some press: the costs of checking home buyers' credit histories. According to the Mortgage Bankers Association (MBA), costs of these may rise by 40% to 50% during 2026.

The MBA has asked the FHFA to allow lenders to rely on a single credit report instead of the common "tri-merge" report when approving borrowers with a 700 or higher FICO score, helping keep costs lower.

The reason why tri-merge credit reports are mandatory is because of the part they play in the secondary loan market. Lenders selling mortgages to Fannie Mae and Freddie Mac must use a tri-merge report as these are mandatory for these transactions.

If you're working with prospective buyers who would like to learn more about closing costs, or other details of the home buying process, I can walk them through their financing options.4

Picky, Nervous Buyers Cancel More Agreements

Based on a Redfin analysis of MLS pending sales data, nearly 40,000 sale agreements nationwide were canceled during January 2026, equal to 13.7% of homes that went under contract that month. That's up from 13.1% a year earlier.

Buyers are more apt to put the brakes on a purchase if the property has any inspection issues, or if they find another home they like better. Cancellations are most prevalent in metro areas where sellers most heavily outnumber buyers. For example, the metro area that saw most purchase cancellations last month was San Antonio, Texas, where there are twice as many sellers than buyers.

In addition, the current atmosphere of economic uncertainty has given some buyers jitters. Some cancel purchases as they've become increasingly concerned about financial and geopolitical tensions, or they learned of planned layoffs that may affect them.5

Sources: 1zillow.mediaroom.com, 2cnbc.com, 3topagentmagazine.com, 4cnbc.com, 5redfin.com

Recent Comments